The Next 'Generation' of Fintech Automation

Just another generative AI thought piece.

The financial services are no stranger to automations. AI and ML are already used in everything from underwriting to fraud detection and compliance. Given that the language of finance is predominantly textual, the disruptive promise of Large Language Models (LLMs) seems obvious. One can imagine popular ideas such as co-pilots and chatbots applied in financial contexts to great effect.

And yet… we haven’t seen fintech startups proliferate through generative AI market maps. So where are they? I decided to take a deeper dive.

First off, finance is a traditionally conservative industry. Some of its systems haven’t changed for literally decades. In my reading, I was surprised to find the 1959 edition of COBOL, Common Business-Oriented Language, is still widely used in insurance and fintech. Despite being incredibly difficult to work with, more than 95% of ATM swipes and 43% of banking systems are written in Cold War-era COBOL. That’s not to say that we can’t expect innovation from the industry, but rather that it’s tempered.

Fintech treads cautiously, and with good reason. Quite apart from regulatory scrutiny, the business models of financial services companies require unique precision to avoid disastrous costs. Tasks such as compliance checks (AML, KYC), underwriting and accounting must be error-free. Unlike most RBL-based AI that’s currently being used in compliance/AML, LLMs are by their nature a black box. The lack of explainability results in significant liability issues. While LLMs might get you 90% of the way, this is an industry that demands 100% accuracy.

Unlike generating content marketing or even code, it seems unlikely that LLMs will form the entirety of fintech products in the near term. Popular foundation models were trained on publicly available datasets, which did not include financial services data. Hence, wrappers around ChatGPT produce results that are too generalized for finance. Likewise, for obvious reasons, data privacy is also a key concern. Already, large financial enterprises like JP Morgan and Goldman Sachs have decided to ban the use of LLM tools like ChatGPT over data leakage concerns. As LLMs benefit from improved data quality, it seems increasingly likely that for fintechs, on-premise hosting will be favored.

A generative revolution?

That doesn’t, however, mean that generative AI can’t be useful in fintech products. Rather, I believe that the next generation of fintech companies incorporating LLMs look different to this initial set of generative apps. In addition to this, the best fintech LLM products are likely to have cross-vertical knowledge or data access. Generative AI might be an ingredient in the end product, but not the full recipe. Below are some examples I’ve come across of where AI components can be useful within broader products or workflows:

Analyzing structured and unstructured data: there is no shortage of documents for financial service companies to deal with. Translating information locked in invoices and contracts into data can be incredibly valuable, but often costly and time consuming. Generative AI unlocks diverse data formats in a way that was impossible before.

Understanding documents is critical for one of Hummingbird portfolio companies, Reiterate, which is using LLMs to extract valuable financial data. One of the company’s core competencies is making sure that when money is changing hands, the amount is correct. The movement of money creates a paper trail - invoices, bank transactions, database entries etc - which can be extremely difficult to understand and correlate. Generative AI allows this process to be fully automated, at scale.

Research continues to be one of the most important functions of many finance teams, whether it's for making investment decisions or understanding consumer willingness to pay. A few interesting companies working on improving the research and search experience on both internal and external data include: Hebbia, Pathway, Kodex, Theia Insights, Rose and EmberML

Validating & Collecting Information: many financial services processes require huge amounts of information collection. In the past ML has started to chip away at this problem, but today generative models can achieve much more.

One example is in compliance, where collecting, organizing and summarizing information is critical. Greenlite, for example, is using generative AI to help analysts be more productive with tasks like transaction monitoring and onboarding. AI-augmented compliance has the potential to remove tedious tasks and let professionals focus more on analytical decision making.

Automating Customer Service: while chatbots in customer service aren’t new, LLMs have the power to create more authentic conversational experiences. For fintechs, this unlocks both cost savings and more engaging user experiences.

Among the many exciting customer service automation companies (both startups and scale ups), a few to watch are Gradient Labs, 8Flow.ai and Intercom’s new chatbot Finn. It’s likely that we’ll see fintechs both building their own conversational experiences with LLMs as well as outsourcing to dedicated third parties.

Personalizing Marketing: playing around with ChatGPT, one thing becomes clear very quickly: it’s extremely adept at writing customized content at scale. LLMs can create personalized messages to promote new products directly to the customer, engaging them on an individual level. For fintech companies, this precision marketing might be able to significantly contribute to upsells and reduce CAC.

The Co-Pilot Model: given that the accuracy of LLMs remains a significant hurdle for finance applications, it makes sense to keep a human in the loop. At a high level, the co-pilot model can improve financial productivity by acting as an assistant while allowing someone to check its work. An example of this approach in finance is Basis, a product that doesn’t seek to fully automate accountants but rather augment their work.

AI Chatbots & Conversational UI: LLMs have brought chatbots back into fashion. Now, for the first time, these conversational interfaces are able to dynamically provide answers and analysis on a diversity of datasets. This means users can start better understanding their financial data:

For example, Pigment, the real-time business forecasting and strategy platform, has used generative AI to create a conversational interface between users and their business data. In this case, a platform that might be traditionally used exclusively by a finance team can start to reach broader audiences across an organization as team members can query in natural language.

In a recent hackathon, Tola ran an experiment to see what GPT-4 could do in accounting and finance (the demo can be found here)

Incumbents versus new challengers

Across multiple sectors, there’s been considerable talk about the significant advantage established players have over newcomers. In fintech, this comes down to data.

As previously mentioned, one of the major hurdles for startups hoping to use generative AI is relevance. Fine tuning models on relevant financial data is critical to creating relevant workflows with LLMs. Bloomberg, for example, has already shown one natural advantage incumbents have over startups; namely their data access. The recently released BloombergGPT was able to outperform similarly-sized open models on financial NLP tasks by significant margins, without sacrificing performance on general LLM benchmarks. Likewise, J.P. Morgan is reportedly already working on a ChatGPT for investors called IndexGPT, helping individuals pick, analyze and recommend financial securities like stocks, bonds, commodities and alternatives.

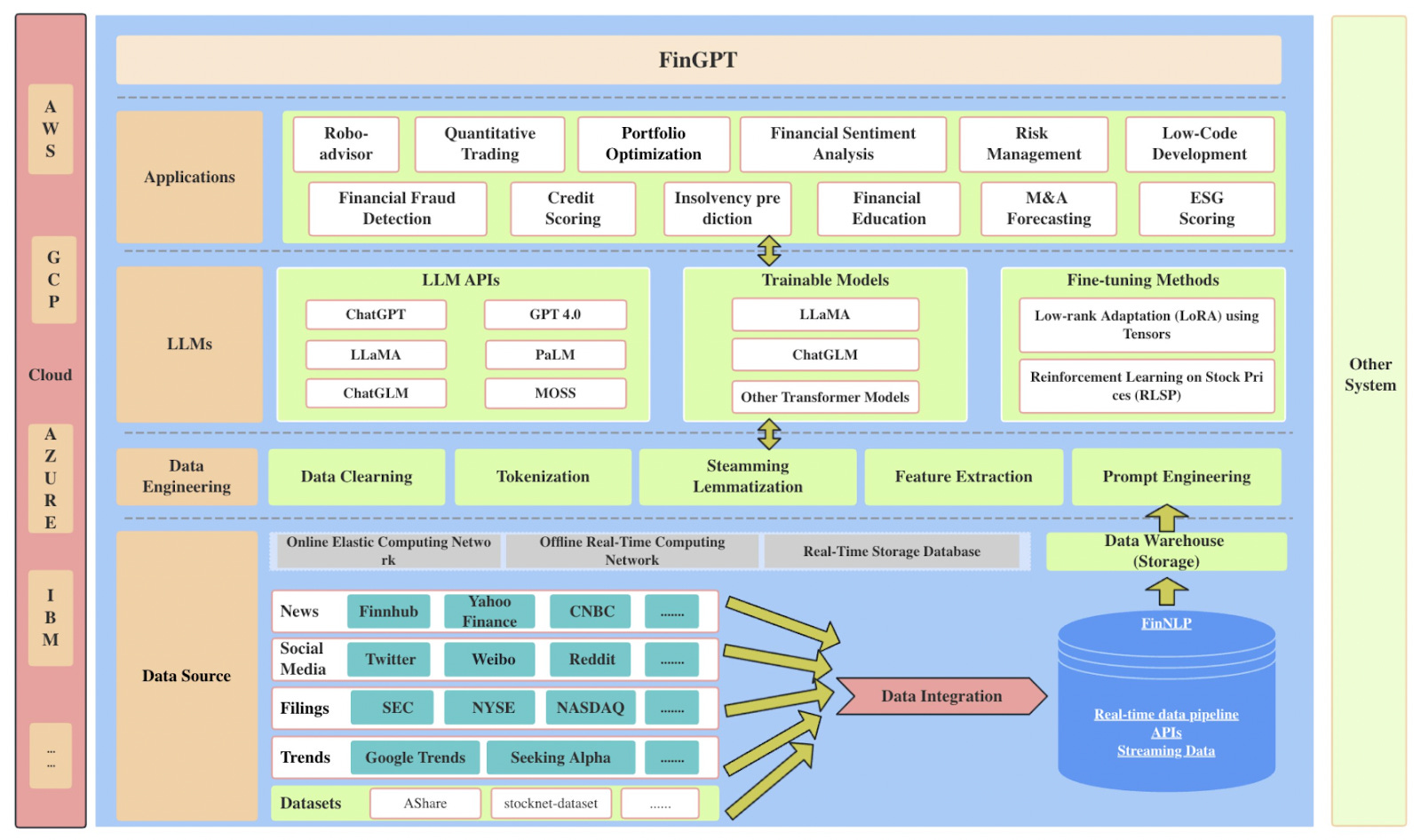

But while data access will initially give incumbents a leg up, it shouldn’t necessarily be viewed as a startup killer. Just this past month, researchers have published an open source large language model, FinGPT, for the finance sector. Unlike proprietary models, FinGPT provides researchers and practitioners with accessible and transparent resources to develop their FinLLMs. The paper goes on to showcase several potential applications as stepping stones for users, such as robo-advising, algorithmic trading, and low-code development.

Conclusion

How far exactly can generative AI go? What might the future of finance look like? One could imagine agents, LLMs that can use tools such as calculators, search, or execute code, optimizing a consumer's financial services experience by switching and getting them the best deals automatically. Many services, such as tax and wealth advisory, are still dominated by humans, who offer a valuable personal or emotional touch in their decision making. LLMs, however, could start to move the needle on understanding complex preferences in the way humans do such as, understanding the tradeoffs between price and quality when budgeting.

Ultimately, we are still very early in this new generation, and I’m incredibly excited by what’s to come. If you’re thinking about building in fintech and tinkering with how generative models might change the status quo, I’d love to hear from you! Feel free to get in touch over email at nikita@hummingbird.vc

Finally, a massive thank you to Firat Ileri, Akshay Mehra, Akshat Goenka, Alex Agus, Tahseen Rashid, Joonatan Samuel, Jimena Nowack, and Felix for their thoughts and feedback on this article.

Super solid!